For many investors, the early years are simple. You contribute regularly, reinvest what the portfolio produces, and trust that time and compounding will do the work. Volatility is tolerated because income is optional and withdrawals are far away.

Then priorities change.

When portfolio income becomes the objective, the operating question shifts. Growth is no longer the goal. Reliability is. The portfolio must now produce cash flow you can live on—without turning every market drawdown into a forced selling event.

This is where many investors realize that while their portfolio may be sound, their income strategy is not.

Why the Accumulation Playbook Breaks Down

Most investing advice is written for accumulation. Buy diversified assets, hold through volatility, and let long-term growth smooth out short-term noise.

That approach works when income is discretionary.

In the income phase, volatility takes on a different meaning. Drawdowns are no longer abstract. They coincide with real expenses and real withdrawals. Advice like “just sell some shares” sounds reasonable—until markets fall and selling begins to feel like liquidation.

The issue is not mathematics. It is behavior under stress.

An income plan that depends on routine selling places the hardest decisions exactly where investors are least prepared to make them.

What “Income Without Selling Shares” Actually Means

Generating income without selling shares does not mean assets are never sold.

It means the portfolio’s baseline cash flow does not depend on scheduled liquidation of principal as the default paycheck mechanism.

Instead, cash flow comes from income produced internally by the portfolio—reducing the need to make discretionary selling decisions during volatile periods.

This distinction matters because strategies that work on spreadsheets often fail operationally when emotions enter the equation.

Why Income-Phase Investors Get Stuck

Most investors reach the income phase with portfolios designed for growth and decision habits formed in calm markets.

Then real life arrives.

Bills are due. Timing matters. Volatility clusters. Withdrawals feel different when they coincide with losses. At that point, investors often respond by underspending, overtrading, or abandoning their own plans.

The fix is not prediction. The fix is an operating model built for income.

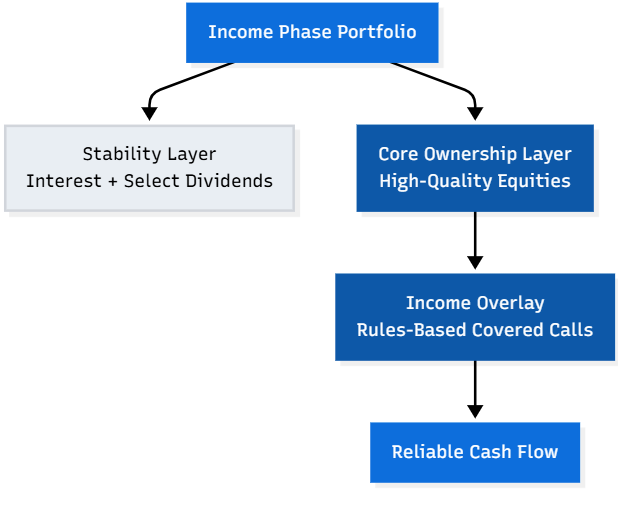

The Three Durable Sources of Portfolio Income

Despite the vast array of income products and strategies, there are only a few durable ways a portfolio can generate cash without routinely selling its core holdings.

1. Dividends

Dividends distribute a portion of company earnings directly to shareholders.

They can be useful, but they are not a complete system on their own. Dividend policies can change. High yields often carry hidden risks. Chasing yield increases concentration and fragility.

Dividends work best as one income layer—not the entire plan.

2. Interest Income

Interest income typically comes from bonds, cash equivalents, and other lending instruments.

Its strengths include contractual structure and lower volatility. Its limitations include inflation risk, interest-rate sensitivity, and credit risk.

Interest income provides stability, not a replacement for equity-based cash flow.

3. Option Premium on Long-Term Equity Holdings

This is where clarity or confusion usually emerges.

Option premium is not free money. It is compensation for accepting a defined obligation. In income-focused portfolios, this often takes the form of covered calls.

- You own shares you intend to hold.

- You sell call options against those shares.

- You collect premium as income.

- Your upside is capped above the strike price during the option’s life.

When used intentionally, this converts volatility into cash flow. Volatility is not just noise—it is often the pricing environment that funds the paycheck.

When used carelessly, covered calls become a stress amplifier, especially when investors sell ceilings they are not emotionally prepared to honor.

Designing an Income Portfolio Without Liquidation Pressure

Income portfolios work best when treated like operating systems with defined layers.

The objective is not to maximize yield. It is paycheck quality—cash flow that is stable enough and emotionally livable enough to maintain through volatility.

The Most Common Income Failure Modes

Income strategies fail predictably when investors chase yield, improvise rules, or sell option strikes they do not truly mean.

Income reduces the need to sell. It does not eliminate risk. Without governance, income can actually increase stress by forcing decisions on a schedule.

Income Is Governance, Not a Product

Durable income systems rely on written rules:

- What you own and why

- What you are willing to sell, and at what prices

- How positions are sized

- What actions you take during volatility

- What actions you never take

Without governance, the market writes the rules—usually at the worst possible time.

Learn the Full Framework

A complete framework for designing portfolio income without selling shares explains how income-phase investors reduce forced liquidation, manage volatility, and align income with behavior.

That framework outlines what these strategies do, what they do not do, and where they fail when governance is missing.

Final Thought

The transition to the income phase is not just financial. It is behavioral.

Portfolios that generate cash internally – rather than relying on forced selling—tend to be more stable, more livable, and easier to sustain across market cycles.

The goal is not perfection.

The goal is durability.